Strong St. Cloud-area outlook clouded by inflation concerns

As the pandemic subsides, the new year has ushered in a long-awaited, broad-based area economic expansion. Virtually all sectors of the St. Cloud-area economy experienced employment growth as the area added more than 3,600 jobs in the year ending January 2022.

Firms’ future outlook remains very strong, but is clouded by accelerating inflation (and accompanying wage pressures) and persistent labor shortages.

Data released by the Minnesota Department of Employment and Economic Development (DEED) indicate St. Cloud area employment increased 3.6% over the 12 months ending January 2022 (but is still 3,144 below its pre-pandemic level two years ago). Local job growth occurred in virtually all sectors, with leisure/hospitality leading the way with a 22.3% employment increase over the past year. Employment in the mining/logging/construction industry also rose 13.8% over the same period.

The St. Cloud Index of Leading Economic Indicators rose 1.7% from three months ago and is 0.8% from its recent high two quarters ago. Five of six indicators rose in the last quarter.

Business activity at surveyed firms was solid over the past quarter. 46% of surveyed firms report an increase in business activity over the past three months and only 13% of firms experienced a decrease in activity.

The future outlook of surveyed firms is very strong as 72% of survey respondents expect improved business conditions over the next six months and only 3% of firms anticipate decreased activity.

In our first special question, most firms indicate hiring practices have been unchanged over the past 12 months (although 28% of firms note that they are utilizing less stringent experience requirements than one year ago). In a second special question, 54% of surveyed firms report they plan to undertake capital spending in 2022 in order to keep up with technology. Another 46% of firms indicate capital purchases are used to produce output more efficiently, while 39% are simply replacing worn-out capital. 25% of firms plan to purchase capital in order to contain labor costs.

In this quarter’s final special question, firms report on the ways in which inflation is affecting their firm. Several firms indicate significant materials cost increases, accelerating wages, and declining profit margins.

Key takeaways from the Quarterly Business Report

1. Private sector payroll employment in the St. Cloud area rose 3.5% from one year earlier in the 12 months through January 2022. The unemployment rate in the St. Cloud area was 3.8% in January 2022, which was much lower than the 5.5% figure observed one year ago (when many social distancing measures were still in place). The local labor force rose by 2.9 percent over the past year, with 3,145 more adults working or available for work in the St. Cloud area than one year ago.

2. Nearly all area sectors experienced employment gains over the year ending January 2022. Sectors with the largest job gains include leisure/hospitality (22.3%), mining/logging/construction (13.8%), other services (5.5%), and local government (7.8%). The only local sectors experiencing job loss were over the past 12 months were financial activities (-0.1%), federal government (-2.0%), and state government (-0.2%).

3. The St. Cloud Index of Leading Economic Indicators rose by 1.7% in the current period. Three of the six indicators rose and three others fell in the current quarter. The St. Cloud 12 Stock Index fell 2.2% over the three months ending Jan. 31, 2022, roughly in line with a 2.0% decrease in the S&P 500. Only two stocks in the index closed higher over that period.

4. The future outlook of area businesses that responded to the St. Cloud Area Business Outlook Survey was stronger than usual for this time of year, as surveyed firms remain optimistic about economic performance over the next six months. 72% percent of surveyed firms expect an increase in business activity over the next six months (and 3% expect decreased activity). 59% of surveyed firms expect to expand payrolls by August 2022 and 74% anticipate increased prices received over the next six months. 69% of surveyed firms expect to pay higher wages and salaries by August. The local labor shortage is a major concern for area firms. 41% of surveyed firms expect it to be more difficult to attract qualified workers over the next six months and only 5% expect these difficulties to decrease.

5. In a special question, most surveyed firms report unchanged hiring practices over the past year, although 28% indicate less-stringent previous experience requirements. In a second special question, 54% of firms plan to undertake capital spending to keep up with technology, while 46% will do so to produce output more efficiently. A quarter of firms said they were using capital to help economize on labor. Firms also commented on how they are being impacted by inflation in this quarter’s final special question.

With a labor shortage, what’s happening with wages?

Sometimes you see a number and think there’s something wrong. Figuring out why can sometimes tell you something surprising.

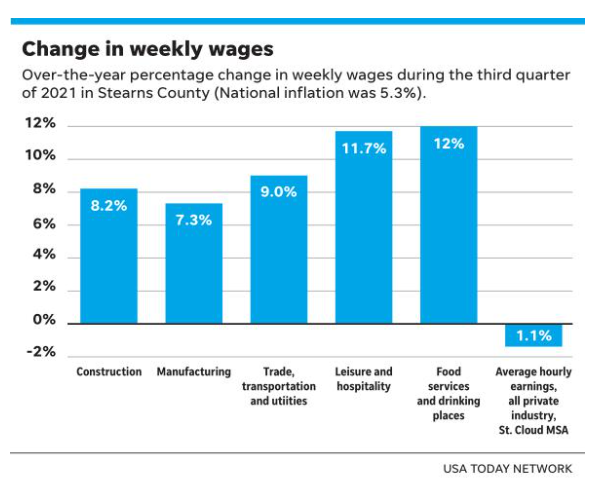

We saw one that is very misleading: Average hourly earnings in the St. Cloud MSA in December 2021 were $25.75, down from $27.32 in December 2019. How, one might think, could wages be going down while we are experiencing a labor shortage?

We learn in today’s report that the leisure and hospitality sector had an employment jump of 22.3% in the 12 months leading to January 2022. It is the largest rise of any sector, with construction rising 13.8% and other sectors much less. One thing we know is that leisure and hospitality contains many lower-wage jobs.

A better way to see what is happening when the composition of the labor force is changing so dramatically is to look at wages by sector. We are too small a community to have monthly data on wages like we do for employment. However, there is another census of employers that allows us to see weekly wages and employer payrolls by sector. The data is not very timely but we can see what the differences were in the third quarter of 2021 by sector. We chose to focus only on Stearns County because aggregating the two counties of the metropolitan statistical area is not possible.

There is a significant amount of variation in the data by sectors for the four we chose to look at. In construction, where employment in the St. Cloud area has grown significantly during the pandemic, weekly wages grew by 8.2% between the third quarter of 2020 and the third quarter of 2021. For that same period, manufacturing rose 7.3%. Employment in manufacturing has not grown nearly as fast.

In the leisure and hospitality supersector, weekly wages grew 11.7%. We should note that weekly wages can rise either because of a rise in the wage rate or a rise in the number of hours worked. Part-time employment is more common in leisure and hospitality than most other sectors. Within leisure and hospitality, the food services and drinking places sector rose a little more, to 12%.

In all cases, the rise in weekly wages certainly is higher than the national inflation rate for that period, which was 5.3%. The inflation rate has accelerated since then, but we do not know what has happened to weekly wages in that period.

These higher weekly wages can be a good sign of a strengthening leisure and hospitality sector if they are supported by robust sales. However, we know that in the St. Cloud, food and beverage tax receipts are still not where they were pre-COVID pandemic. Thus it seems likely that the labor shortage in that industry is quite real, wages are rapidly rising as a result, leaving restaurant operators in the middle.

QBR: Survey results for standard questions

Current St. Cloud-area activity

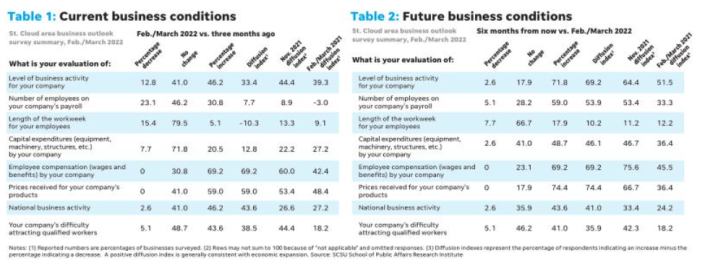

Tables 1 and 2 report the most recent results of the St. Cloud Area Business Outlook Survey. Responses are from 39 area businesses that returned the recent mailing in time to be included in the report. Participating firms are representative of the diverse collection of businesses in the St. Cloud area. They include retail, manufacturing, construction, financial, health services and government enterprises, both small and large. Survey responses are strictly confidential. Written and oral comments have not been attributed to individual firms.

Table 1 shows that business activity during the three-month period ending in February/March 2022 was slightly weaker than one year ago. However, the employee compensation and prices-received indexes are considerably higher than were recorded last year (which was a time when inflationary pressures were just beginning to appear).

For example, the diffusion index on employee compensation is 69.2 — the second-highest reading ever recorded. By comparison, one year ago the current employee compensation index was 42.4. A diffusion index represents the percentage of respondents indicating an increase minus the percentage indicating a decrease in any given quarter. For any given item, a positive index usually indicates expanding activity, while a negative index implies declining conditions.

Index values on national business activity and difficulty attracting qualified workers were also elevated this quarter. 44% of firms report increased difficulty attracting qualified workers this quarter and only two firms indicate the local labor shortage has moderated.

The one puzzling result from Table 1 is the item on current capital expenditures (see accompanying chart). At a value of 12.8, this index is at its lowest level since the onset of the pandemic recession. We note that this performance is not seen in the future conditions index (Table 2). Capital spending plans over the next six months are relatively strong.

As always, firms were asked to report any factors that are affecting their business. These comments include:

-

High and volatile material prices and long lead times. Damaged products when the product arrives. Very little quality control.

-

Taxes and overregulatiion.

-

Talent acquisition and retention.

-

The Biden administration has turned into a train wreck for the American economy and business.

-

Supply chain issues.

-

LABOR!!

-

It’s currently all about labor, labor, labor. More business to be had, but can’t due to labor constraints. I don’t know if/how/when that situation improves.

-

We are concerned about the trends we see in enrollment at St. Cloud State University and the criminal activity that seems to be taking place around the SCSU campus. We believe these trends will have a negative impact on our community.

Future outlook

The results from the future conditions survey in Table 2 are among the strongest ever recorded over the 24 years that the survey has been administered. For example, the future business activity index (see accompanying chart) is 69.2, its highest reading since March 2000. 72% of surveyed firms expect improved business activity by August, and only one firm expects weaker conditions, so there is considerable reason to be optimistic about local economic activity over the next six months.

The future capital expenditures index was also strong this quarter. 46% of firms expect higher capital spending over the next six months and only one firm expects to reduce capital purchases. Special question 2 (found elsewhere in this report) suggests these planned capital purchases are typically intended to help firms keep up with technology as well as to improve productive efficiency.

With 59% of surveyed firms expecting to expand employment by August (and only two firms expecting decreased payrolls), the future employment index is at its highest recorded level in more than 20 years. Ongoing worker shortages and a low local unemployment rate make it unclear where area firms are planning to find workers, but they expect to provide higher employee compensation to attract (and retain) workers over the next six months.

The diffusion index on future employee compensation is 69.2. No surveyed firms expect to pay lower wages and salaries by August. The prices-received index also remains elevated. Almost three-fourths of surveyed firms expect to receive higher prices by August and no firms expect prices received to decrease. The diffusion index on this item is once again the highest ever recorded (see accompanying chart).

As we noted last quarter, the worker compensation and prices-received indexes have been historically correlated with improved local company performance, but the current period may be different. To the extent that these figures reflect supply chain bottlenecks and/or general inflationary pressures, these responses may not be a favorable local indicator. Responses to special question 3 address these concerns.

This quarter’s final survey chart looks at the future difficulty attracting qualified workers index. The value of this series is 35.9, which is lower than in the previous three quarters. This may suggest a moderating local labor shortage, but we will need a couple more survey readings to know if this is the case. We do note that the local labor force actually increased (by 2.9%) over the past year, so this could be helping to reduce area firms’ difficulty attracting talent.

QBR: Special questions reveal few changes in hiring practices around St. Cloud area

The COVID-19 pandemic has forced firms to reinvent business practices across the entire range of company activities. Among these practices are those that relate to managing the company workforce. As labor demand increases and telework options become more popular, we thought it would be useful to see how specific hiring practices may have changed over the past year. We asked:

SPECIAL QUESTION 1: Over the last 12 months, which of the following adjustments have been made in the qualifications your firm uses in its hiring practices?

Most surveyed firms report unchanged hiring practices over the past 12 months. The one category in which less stringent hiring practices seem to have emerged is in prior experience requirements. 28% of firms indicate they have relaxed previous experience requirements in the past year. Written comments include:

-

We have made no changes. The requirements for new employees are needed for us to do our work.

-

We end up training a lot more after being hired than before. Less qualified or motivated workers.

-

We no longer drug test. Not enough candidates to be picky.

-

Already became as lenient as possible more than a year ago. To no avail. A pulse and a willingness to show up is about all it takes … and still positions go unfilled.

-

We have eliminated drug testing in our manufacturing plants due to the number of otherwise good applicants who test positive for THC [the active ingredient in marijuana].

-

We’ve always used background checks and drug screenings.

-

Great talent is available (at higher cost).

-

Capital spending plans for area firms

SPECIAL QUESTION 2: Which of the following represent goals your firm has in its capital spending plans in 2022 (Please select all that apply)

Our second special question addresses firms’ capital spending plans in 2022. We already noted in tables 1 and 2 that local companies limited their capital purchases over the past three months (which could be a seasonal effect as well as reflect ongoing supply chain issues) but expect fairly robust capital spending over the next six months. A commitment to capital spending is a sign of a healthy economy, so we are encouraged by these strong future business conditions survey results. Of course, reasons for capital expansion are varied, so we thought we would ask firms about their goals for capital expansion this year. Note that surveyed firms were requested to select all applicable responses, so percentages total up to more than 100%.

The most popular reason for capital expansion is “keeping up with the latest technology.” 46.2% of firms indicate their planned capital purchases are to increase productive efficiency and another 38.5% of firms are replacing worn-out capital.

One way of addressing persistent local worker shortages is to substitute capital for labor. 25.6% of surveyed firms identify this as an objective of their capital spending plans this year.

Finally, 15.4% of firms are acquiring new capital in order to “enter a new product area or service space.” A few firms provided written responses. These include:

-

Other — technology for new hires.

-

These are our standard capital purchasing requirements.

-

Always trying to stay ahead and keep equipment all serviced or updated as feasible.

-

We always need to look at new products on the market.

-

Switching to digital press technology to eliminate need for trained press operators.

-

Many of our experienced trades workers are aging out of the workforce. We are looking at a new construction practice that requires less skilled labor as we have had zero success to replace (retiring workers).

-

Wage increases make exploring and adding technology more important and more affordable.

-

Adding capacity.

-

No capital plans for 2022 at this time.

Let’s talk inflation

U.S. inflation rates have been elevated for the past year as aggressive monetary policy targeted at promoting high employment has collided with supply chain difficulties and lower labor force participation to produce inflationary pressures. For example, over the year ending in February 2022, the Bureau of Labor Statisitics (among other things, they maintain the Consumer Price Index — the CPI) reports a 25.6% increase in energy costs, a 12.4% increase in new vehicle prices, and a 41.2% rise in the prices of used cars and trucks. The overall CPI rose 7.9% over the year ending February 2022 and the closely watched core CPI (which subtracts food and energy prices) rose 6.4%.

In the long run, inflation is a monetary phenomenon. So, after materials, product and labor supply conditions return to “normal” in a post-COVID economy, the Federal Reserve will need to use its monetary policy to tame inflation and contain inflationary expectations.

The Fed has been willing to trade off some “transitory” inflation increases over the past year in an attempt to use expansionary policies to achieve its high employment mandate.

But now that national labor markets have stabilized (for example, the national unemployment rate is now 3.8% — considerably lower than the 6.2% reading from one year ago), it is time for them to try to get inflation rates back to their 2% annual target. The Fed’s targeted measure of inflation — the Personal Consumption Expenditures (PCE) deflator — has not increased as rapidly as the CPI over the past year (it rose at a 6.3% annual rate in the fourth quarter of 2021), but it remains elevated above the 2% target.

By the time this report appears in print, the Fed had begun to increase the target for its key interest rate (the federal funds rate) as it begins to tighten up on monetary and credit conditions. This more restrictive interest rate policy is expected to proceed over the rest of 2022 (and into 2023) until monetary policy has returned inflation rates to their longer run values.

It is beyond the scope of this report for us to debate the extent to which these efforts will be successful, but we think most people agree that it is time for the Fed to get moving on containing inflationary expectations by restraining its monetary policy actions.

With these concerns in mind, we thought we would ask area firms an open-ended question about how inflation was impacting them. Area companies note that inflation is causing higher wages, increased materials costs, more aggressive pricing, and, in some cases, reduced profit margins. We asked:

SPECIAL QUESTION 3: Please comment on the ways in which inflation is impacting your firm.

We let the survey responses tell the story:

-

The present changes may force customer fee increases.

-

It sucks, to put it in plain English. Need to get gas/energy prices under control. Do that and prices will come down along with inflation.

-

Driving the cost up on materials to a point where some customers are looking at repairs instead of (product) replacement.

-

Much higher wage increase to retain staff. Increased annual (cost of living) base pay increase from 2% to 5% plus merit increases.

-

Forcing wage growth for retention.

-

Inflation is hitting us from every direction and starting to affect consumer buying decisions. If this continues at this pace we will see the economic effects like 1979-82 once again.

-

Higher labor costs.

-

Costs are going up everywhere. Nothing is going down. We would normally raise prices annually. We are now raising prices more frequently just to stay in sync with costs.

-

Paper is up 30%, plates, ink and other consumables up 10-25%.

-

Projects that are ongoing have had material price increases that we cannot charge for as we have guaranteed price contracts.

-

Metal (hot-rolled and cold-rolled) was arguably among the earliest and biggest inflationary flashpoints, having risen several hundred percent in 2021. No choice but to pass on. Mostly successfully, but some contract obligations still existed at “old” pricing. Everything else has been relatively minor and easier to deal with in comparison.

-

It is increasing our cost of goods, profit margins and labor costs.

-

We work under fixed price contracts so we have passed on some projects that have long delivery times. Delivery times are really impacting work going forward with a window up to 6 months…

-

Virtually every cost from raw materials to packaging to fuel and shipping costs is increasing by large percentages, driving up the price of our products to customers.

-

Cost of goods.

-

We are strongly dependent on transportation. We ship 30-40 semi loads of material monthly. The inflation rate on fuel is drastically affecting our profitability.

-

Inflation is in every area we do business. This is by far the worst and fastest inflationary growth we’ve seen. Add wage increases into the mix and we see this as a long-term issue.

-

It has been difficult to pass on costs in a timely manner.

-

Increased freight costs — in and out.

-

Federal Reserve plans to increase federal funds rate — which will push up loan and deposit rates (in the banking industry).

-

The only impact from inflation has been a need to increase wages more than in the past.

-

Prices are roughly 20-30% higher. Wages and labor costs have been increased intentionally.

-

Price increases significant — 20-25%.

-

Raw goods costs have increased a lot over the last two months.

-

Decreasing our bottom line.

-

Prices have had double-digit increase.

-

Significantly driving up wages, which requires our firm to increase our prices.

-

It’s making my clients very nervous!

-

Outsourced and in-house labor costs are up 20-25%.

-

Inflation is causing us to increase prices and threatening to erode margins.

-

Cost of products has increased. We increased employee wages to try to avoid losing people and to make them happy.

Leading indicators confirm rising Central Minnesota business expectations

Based on revised data from the Minnesota Department of Employment and Economic Development shown in Table 3, employment the St. Cloud Metropolitan Statistical Area grew 3.6% in the 12 months ending in January 2022. This was higher than the Twin Cities MSA and the state as a whole; St. Cloud edged out Duluth and Rochester to have the fastest-growing employment in the state.

For this to happen while growth in the St. Cloud manufacturing sector was below growth in the rest of the state is all the more remarkable. DEED notes that average annual job change between 2020 and 2021 was revised downward to 1.1% from 1.5%, for a change of 401 fewer jobs than previously reported.

Two sectors that have grown rapidly over the last year are construction and leisure and hospitality. The latter is easy to understand since the numbers are growth from the industry-wide closures of restaurants in January 2021. In the other case we continue to see growth in the construction sector driven by both growth in commercial and residential structures. Data from the Central Minnesota Builders Association (not shown) showed building permits at their highest level since 2016, particularly for building in Sartell.

Save for a drop of 6 jobs in the financial sector, every private industry in the St. Cloud area experienced an increase in jobs. Notably, wholesale and retail trade rose in St. Cloud while declining elsewhere in Minnesota. Area employment at the federal level was down 2% and state-government employment was down a small fraction.

As shown in Table 4, the St. Cloud area labor force grew 2.9% in the 12 months to January 2022. In the previous 12 months it had fallen by 3%, so the area labor force is 295 persons less than January 2020. Of the five Minnesota MSAs, only Rochester has a greater labor force in January 2022 than it had in January 2020.

Thus while the unemployment rate in St. Cloud in January at 3.8% was higher than the state or the Twin Cities, this may not be a bad thing. It indicates that there are relatively more workers actively seeking employment in the area.

After the end of extended unemployment insurance benefits in September 2021, initial claims fell in the St. Cloud area. … (needs data, this is a placeholder for something I will write.) Building permit valuations in the St. Cloud fell slightly in this period.

St. Cloud stock index up sharply

The St. Cloud Stock Price Index rose by 30.4% in the 12 months to Jan. 31, 2022, though it fell 2.2% in the final three months of that period.

By comparison the S&P 500 rose 22.1% over the 12 months and fell 2.0% in the final three months. During this period we removed Newell Brands from the index as it wrapped up operations of Stearns Manufacturing at the end of 2021. This marks the second stock removed in as many quarters, as Brookfield Property Group left our index at the end of July. We will re-evaluate the index to determine if other stocks can be included. Of the remaining 10 stocks, two rose in the last three months, C.H. Robinson and Encore Capital Group.

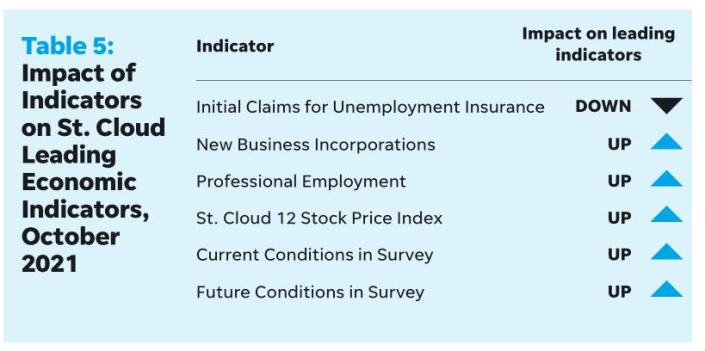

Five of the six elements of the Index of Leading Economic Indicators rose in the last quarter. Only initial claims for unemployment insurance in the MSA detracted from this measure. The survey responses, particularly to current conditions, and improving professional employment (which includes the bellwether temporary jobs category) contributed most to the reading this time.

We note that this report was written after the invasion of Ukraine by Russia, and some of the responses to the St. Cloud Area Business survey were written with knowledge of that. We also are writing this report on the eve of what Federal Reserve Chair Jay Powell has said will be the first interest rate hike of what promises to be a lengthy process of raising rates and perhaps reducing the Fed’s balance sheet. There are thus many uncertainties in the months to come.

But our read of survey responses and data are that the local economy has exited the omicron wave of COVID-19 with slight improvements in labor availability and strong expectations for growth among area business leaders, with plans to add both capital and labor in 2022.

This article originally appeared on St. Cloud Times: Quarterly Business Report: Strong outlook clouded by inflation concerns